Maine insurance rates remain among the lowest in the US. But home and auto rates are up as insurers struggle with rising claim costs and rising construction values. Portland Maine area insurance buyers saw increasing prices in the 3rd quarter of 2022.

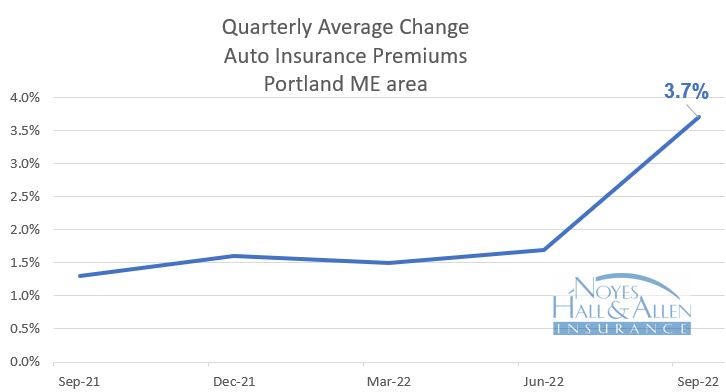

Maine Auto Insurance Rates – June to September

Between June and September 2022, Portland Maine area auto insurance rates averaged a 3.7% increase at renewal, up from 1.7% last quarter. That’s still below the national average of 4.3%.

About 62% of auto insurance buyers experienced an increase in premium. The other 38% saw premiums the same or less than before. Higher repair costs, delays finding replacement parts and increased driving speeds are all factors insurance companies site when they have to increase rates. Customers’ rates might decrease if accidents and violations “age off” or they choose to reduce or remove coverage on vehicles.

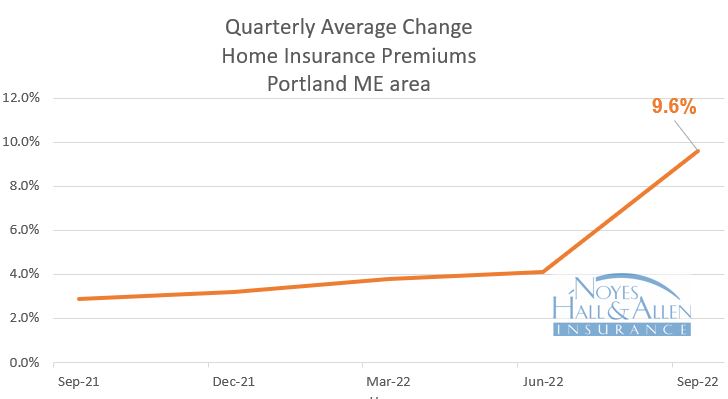

Maine Home Insurance Rates – June to September

Portland Maine home insurance renewal rates increased 9.6% from June to September. That’s rising faster than auto premiums, and an increase from last quarter’s 4.1% clip. That’s still less than the national average.

Home owners were more likely than auto insurance customers to see a rate increase: 91% saw a renewal increase. Only 9% saw rates stay the same or decrease. Higher building costs contributed to increased rates. So did longer rebuilding times due to labor shortages. The cost to rent temporary housing is very high now. That drives property insurance rates higher. So does the increasing cost of property reinsurance. That’s affected by disasters and other uncertainties.

Maine insurance rates are some of the lowest in the US. But home and auto rates are up as insurers struggle with rising claim costs and rising construction values. Fortunately, Maine insurance buyers are seeing smaller rate increases than much of the country.

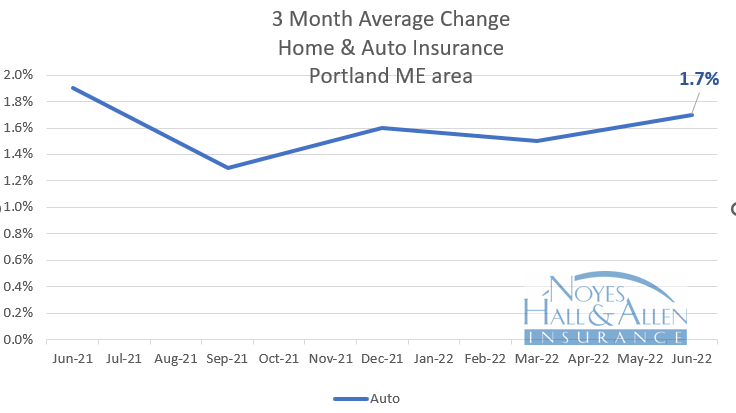

Maine Auto Insurance Rates

As of June 2022, Maine auto insurance rates are averaging a 1.7% increase at renewal. That’s considerably less than the national average of 4.3%. The Wall Street Journal recently reported increases as high as 20%.

The main factors driving auto insurance increases include:

More driving. Miles driven are returning to near pre-pandemic levels

More serious crashes. Traffic fatalities reached a 16-year high last year.

Higher repair costs. Parts and labor costs have both risen sharply due to staffing issues, shipping problems and supply chain glitches.

Higher used car prices. When insurance companies total a vehicle, they have to pay the current used car market price. Used car prices went through the roof recently.

Car rental issues. Auto body repair times are much longer. That means longer replacement rentals. Daily car rental costs have spiked, too.

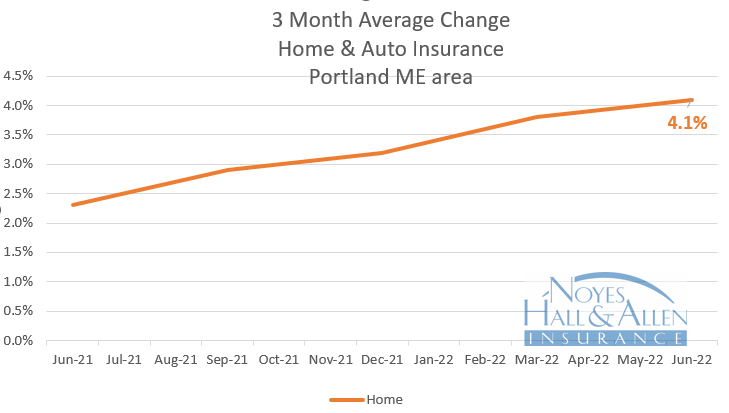

Maine Home Insurance Rates

Maine home insurance rates are rising faster than auto premiums, at a 4.1% clip. That’s still less than the 6% national average. And at an average premium of $1005 per year, Maine home insurance is a relative bargain.

Home insurance costs are affected by building values and claim costs.

Rebuilding costs. Building materials and labor costs spiked during the pandemic. Insurance companies have increased their “inflation guard” factors to provide increased coverage on renewals.

Longer repair times. Contractors are hard to find, too, which increases additional living expenses.

Unusual weather.Natural disasters caused $116 Billion in insured claims in 2021. Maine sees far less than the rest of the US. That’s one reason why our rates are lower. But insurers are feeling less certain about predicting future losses.

Individual Home and Auto Insurance Rates Vary

Every insurance company files their rating plan with the Maine Bureau of Insurance. That plan includes individual rating factors such as driving record, insurance claim history, property location and personal insurance scores.

Does car insurance include roadside assistance in Maine? It’s a common question.

Off the shelf auto insurance policies do not include roadside assistance. But many insurance companies offer it as an option. Others offer towing coverage. Both are less expensive that auto club options.

Are Roadside Assistance and Towing Insurance the Same?

Insurance companies have offered towing coverage for years. Roadside assistance is newer. They’re not exactly the same thing.

Roadside assistance and towing cover many of the same things. Examples are: flat tire repair; jump starting; fuel delivery; and towing, of course. The difference is that towing coverage reimbursesyou after the service call. You have to arrange your own service provide. Coverage is limited to a flat dollar amount, often $75.

Roadside assistance is a service. You don’t usually pay at the scene. If you need assistance, you call a special number and provide your policy info. Some insurers have their own app that you can use to summon help. They dispatch a truck to come and help you. Some roadside plans have a dollar limit per disablement. Most use a towing distance limit – often 25 miles.

How Much Does Roadside Assistance Cost on an Auto Insurance Policy?

Each insurance company sets its own rates. In Maine, expect to pay between $10 and $20 per vehicle per year for roadside assistance. Towing coverage usually costs less than $10 per vehicle for a $75 limit.

Do You Need Roadside Assistance or Towing Coverage if You Have AAA or Onstar?

Most people choose not to have both. They either buy roadside assistance on their auto insurance, or another road service.

Some clients choose to buy towing insurance even though they have another service. For example, some subscription plans charge extra to tow more than 25 miles. If that happens, they pay the excess and submit the bill to their insurance under towing coverage.

Answers to Maine Auto Insurance Questions

Live in southern Maine? Have questions about roadside assistance or auto insurance? Call a Noyes Hall & Allen agent in South Portland at 207-799-5541. We offer a choice of many of Maine’s most popular insurance companies. Many of them offer optional roadside assistance coverage. We’ll help you find a solution that fits your needs and budget. We’re independent and committed to you.

Replacing a car with a new one is an easy insurance transaction. Here’s the info your agent needs to do it:

3 Things Your Agent Needs:

VIN – The Vehicle ID Number for the new vehicle. It’s 17 digits long. That’s easy to transpose. And lots of letters and numbers sound alike, so they’re easy to get wrong. A photo of the VIN simplifies the process and reduces mistakes. Text it to your agent, or email it to them.

Finance Info – Did you buy the vehicle outright? Congratulations! Your agent doesn’t need anything. But if you lease it or take out a loan, they do. The name and address of the finance company will be on your title application. Email or text a photo to your agent. Or, you can call with the info.

Aftermarket Safety or Security Options – The VIN contains details about what’s on your vehicle when it comes off the assembly line. If you purchased add-ons at the dealership, let your agent know. That might include subscription items like OnStar. Or an after-market alarm system.

Do you live in Southern Maine and have questions about auto insurance? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We’re independent and committed to you.

During the COVID-19 pandemic, reduced driving and insurance costs have been a hot topic. Many Mainers are driving less. Why haven’t their car insurance rates dropped? It’s more complicated than you might think. But there are ways to keep your car insurance costs in check.

Why Maine Insurance Rates Haven’t Dropped

Insurance is Slow and Steady

We count on insurance companies to be dependable and stable. We need to know they’ll be able to pay claims in the future. So it’s no surprise that insurance companies aren’t built to react to fast trends. Especially those that may not last.

We want stable insurance prices. The whole purpose of insurance is to avoid a large loss by paying a small cost (premium). Some years, disasters cause insurance companies lose a lot of money. Other times, claims are low. Insurers bank our premiums in those times to pay for the bad ones.

Insurers Have No Experience with COVID

In insurance, data rules. Insurance companies charge premiums based on expected claims. They hire smart math nerds who use decades of data to find the proper rates. Consumers want the lowest possible price. Regulators and stakeholders want rates high enough to make a profit pay future claims.

Historical data didn’t help much during COVID. Americans drove less as people telecommuted and stayed close to home. Nothing was normal.

But overall mileage doesn’t tell the whole story. Essential workers continued to commute as usual (thank you, essential workers!). Law enforcement and highway construction crews noticed increased speeds due to less traffic. That led to more serious crashes and injuries.

COVID Auto Insurance Rebates in Maine

Remember how quiet the roads were in the early days of the pandemic? It was a very uncertain time for the economy. Many people were out of work, and small businesses feared that they’d have to close.

In response, most American auto insurance companies refunded some premium to policyholders in 2020. This was an unprecedented response by insurance companies. By law, rebating of premiums is illegal. But state insurance departments approved exceptions.

But it wasn’t easy. Insurance companies’ billing systems weren’t programmed to rebate money to customers. It was difficult for many of them to calculate and distribute the refunds.

Although the insurance industry returned $10 billion to US consumers, individual refunds were quite small. The public hardly noticed them. Between the underwhelming public response and the cost of the workarounds, insurers didn’t think the rebates were that valuable. We don’t expect rebates again anytime soon.

Reduce Your Auto Insurance Costs When Driving Less

OK, so car insurance companies aren’t slashing rates in response to COVID. And they’re probably not going to refund premium this year. You still have control over your own policy. Here are some adjustments you can make.

Be Sure You’re Properly Rated

Does your policy reflect your actual driving? If you’re working from home, retired or unemployed, maybe not. Check the drivers listed on your policy. Are any of them no longer at home? Do they now have their own insurance?

Check Your Collision Coverage

Do you have an older car that isn’t worth much? Is it rarely driven? Do you have a vehicle that’s completely off the road? Consider removing collision coverage, at least during COVID. Just remember to add it back if the situation changes.

Prove You’re Driving Less

Even “slow and steady” insurance is changing with the times. Several now offer “usage based insurance”. Commonly advertised brands include Progressive Snapshot, Travelers Intellidrive and Drivewise from Allstate.

With usage-based insurance, you allow the insurance company to customize your rate in exchange for an up-front discount. You’ll need a smartphone and the insurance company’s app. Your final price varies depending on how, how much and when you drive. It can be lower or higher than the initial discount.

Safeco Insurance offers a twist: a “low mileage discount” that doesn’t use a real-time monitor. You simply verify your previous year’s mileage to continue to earn their discount. Safeco also has a usage-based mobile app option.

If those cost-saving measures don’t work for you, you can always compare rates with other insurance companies. Live in Greater Portland Maine? You can get up to 5 Maine auto insurance quotes in 10 minutes on our website. Or call a Noyes Hall & Allen agent in South Portland for quotes at 207-799-5541.

We offer the choice of more than a dozen insurers, so we can search the market for the best value. We’re independent and committed to you.

Some car dealers offer Maine car insurance at the time of purchase. This is good for dealers because it increases their closing rate and their profits.

Is it good for you? Maybe not.

If you already have insurance, making a snap decision to change when buying a new car at a dealership can be a bad choice. Here’s why.

What’s the Rush?

The salesperson may create a sense of urgency about insurance. However, there’s no rush. If you have an insurance policy with collision coverage on at least one vehicle, your policy probably automatically covers the new one until you can contact your insurance company or agent. Dealers know this; it’s been that way for decades.

Why Add Pressure?

Car buying is already a stress. Why add more? Most of us don’t make our best decisions under pressure. Moreover, you’re making a big financial commitment and choosing between expensive options on the fly. Don’t let the salesperson force you to make unnecessary snap decisions. That includes insurance.

A “Good Deal” May Not Be

First, many new cars have high-end safety features that help reduce insurance costs. Therefore, some don’t cost any more to insure than the ones they replace. So, if you get a quote at the dealer, and were pleased to see it wasn’t as much as you expected, it may still be more than your current insurance company would charge.

You Can Mess Up Your Other Insurance

Your current policy might have benefits you’ll lose. For instance, a home/auto bundle discount. Or a multi-vehicle discount. Or accident forgiveness, or some other perk. You could lose those if you make a snap decision to insure your new vehicle at the dealer. In conclusion, you might pay more – not less.

You Can End Up With Worse Insurance

First of all, most people don’t know what insurance they have. For example, the liability limits and deductibles on their policy. If they make snap insurance decisions at a dealership, they can end up with inadequate coverage.

In conclusion, if the insurance quote from your dealer is really a better value, that won’t change in a few days. Take your time. Make your insurance decisions on your schedule – not the salesperson’s. Above all, whether you switch insurance or not, you’ll have peace of mind that you made the right choice after a thoughtful decision.

Many Mainers drive less than they did a year ago. By many accounts, we are logging about 30% fewer miles than this time last year. Should insurance companies reduce your car insurance rates as a result? Maybe. But it won’t happen automatically.

Here’s why.

2020 Driving Trends Affecting Car Insurance

Driving data indicates a dramatic change in behavior in Spring 2020. We all know why.

Fewer Miles Driven (but not by everyone). Many people are not working, or working from home. That means they’re driving less, and not as far. But essential workers and others continue to commute. Some people actually drive more than before, replacing lost income with new gigs.

What Rush Hour? With many offices closed, usual morning and evening congestion has almost disappeared. Those who are are driving do so at different times of day, spreading out road usage. That means less risky driving behavior such as hard stops and quick acceleration.

Increased Speeds With more open space on the road, average vehicle speed increased. Faster speeds and clearer roads can mean fewer but more serious crashes.

Is Your Car Insurance Priced Right?

You might deserve lower car insurance rates. But it won’t happen automatically.

Insurers probably won’t reduce rates across the board. That’s because they don’t know who’s driving less than before.

Car insurance often classifies usage into 3 categories:

Pleasure use – used around town and for personal errants. Not driven to work.

Commute – either short (less than 15 miles one way) or long (more than 15).

Business – such as a traveling sales person, trade contractor or other extensive use.

You may deserve lower car insurance rates. But it won’t happen automatically.

Imagine two Scarborough neighbors. One commutes 7 miles on I-295 into their Portland office every day, parking on the street. The other drives 2 miles to teach at a local school, parking in the school lot. In the summer, the teacher doesn’t commute at all.

They’re rated the same, even though their drives are much different. The Portland worker pays too little, while the teacher overpays.

Customized Rating– Gaining Acceptance

New technology allow insurers to customize car insurance prices as never before. It’s called Usage Based Insurance, or UBI.

Using smartphones, customers share driving data with their insurance company. The insurer compares them to other customers. Safer drivers pay less; riskier ones might pay more. Insurance companies have their own brand for UBI: Progressive Snapshot; Safeco RightTrack; Travelers Intellidrive, and so on. Each one has slightly different features.

In prior years, consumers hesitated to share this data, often citing privacy concerns. That changed in 2020. Many are looking for ways to save money in this time of economic hardship and reduced driving. Almost 50% of people who responded to a JD Power 2020 survey were willing to try Usage Based Insurance (UBI).

Are Customized Insurance Rates Right For You?

Think you’re paying too much for Maine car insurance based on your driving? Interested in learning more about Usage Based Insurance? It’s not for everyone.

A Noyes Hall & Allen Insurance agent can help you decide if it’s right for you. We offer a choice of many of Maine’s top auto insurers, with and without UBI. Call our team in South Portland at 207-799-5541. We’re independent and committed to you.

It’s a good idea to compare car insurance quotes periodically. Rates change frequently. The company that was the best value years ago might no longer be.

Car insurance is a big item in many budgets. Saving 5 or 10% can mean $100 or more. So what’s the best way to shop for car insurance?

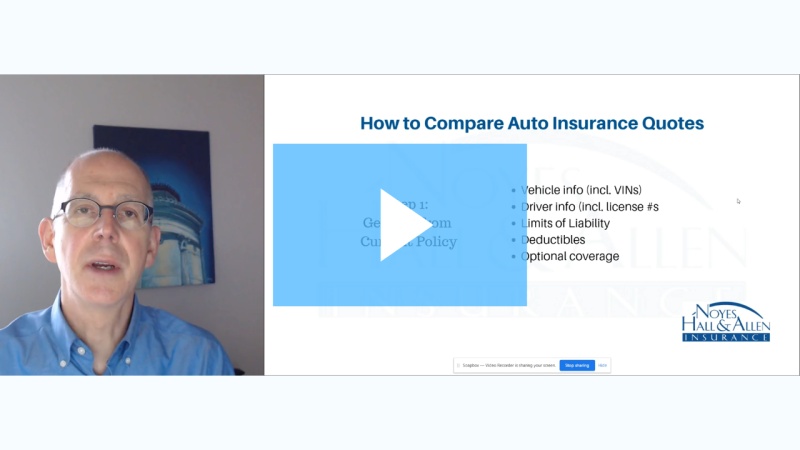

Step 1: Gather Informationfrom Your Policy

You’ll need:

Vehicle description, including VIN;

Driver information (dates of birth, license numbers);

Details about claims, accidents or violations in the last 5 years;

Current coverage limits and deductibles.

Step 2. Decide Where to Get Your Quotes

You have 3 basic options for insurance quotes:

DIY – go online or call an 800 number. You’ll get one quote at a time from a company like GEICO or Progressive. You’ll need to call a few agents to get comparison quotes.

A company agent, like Liberty Mutual, State Farm or Allstate. You’ll still get only one quote. That means you’ll have to call several to compare. But unlike the DIY option, an agent will be able to offer custom advice and answer your questions.

An independent agent, like Noyes Hall & Allen. They provide custom advice and answers like a company agent, with the added convenience of quotes from several insurers at once.

Comparing quotes from different car insurance companies isn’t easy. Each company’s presentation looks a little different. Some may not offer the coverage limits you asked for. And they may not even tell you that it’s not the same.

Step 3: Compare Car Insurance Quotes

This 6:40 video explains what to look for, and what to watch out for.

We Help You Compare Car Insurance Quotes

If you live in Maine or are moving to the Portland Maine area, a Noyes Hall & Allen Insurance agent can help. We represent many of Maine’s top auto insurers. We can explain coverage and price differences to help you find the best insurance value. We’re independent and committed to you. Call us at 207-799-5541, or start an online insurance quote in 10 minutes.

I’ve been testing Travelers’ Intellidrive mobile app. It uses my smartphone to track the quantity, quality, timing and location of my driving. Several insurance companies offer similar apps, including Progressive Snapshot, Allstate and Safeco Right Track. Most offer an up-front discount to try it. They adjust your rates after 6 months to reflect your driving safety.

Travelers allowed me to install Intellidrive without association to an insurance policy. These apps, known as telematics, are becoming more widespread. Clients ask me about them. It’s easier to explain and advise clients if I’ve tried the app myself.

The COVID effect – Are We Driving Less?

Most of us are driving less during COVID time. Insurance companies should give us a break for that, right? Many of them did, with across-the-board refunds in April and May.

But we’re not all driving less. In larger cities, mass transit reductions have forced people to find other ways to get around. Some of us are back to work. Some are working from home; or not working at all. Others are driving even more than before, delivering food or passengers to pay the bills.

The COVID disruption was so fast and intense that insurance companies don’t have a lot of data to adjust rates. That’s why they love these driving monitoring devices.

How Telematics Works

Like most insurance company telematics apps, Travelers Intellidrive monitors:

Time of Day

Number of Miles Driven

Location of Driving

Acceleration, Hard Braking and Speed

Distracted Driving

It’s usually smart enough to know when you’re a driver vs. a passenger (you can re-classify a trip if the app goofed).

Hit all the targets, and you can earn up to a 20% rate cut with most insurers. High-risk driving will cost you a surcharge. The average rate effect for all drivers is minus 5%. Insurers say 70% of customers get some discount.

The app reports how you’re doing. If you don’t like the early results, you can opt out within 45 days without any penalty. You just lose the up-front discount.

Humans are Bad at Estimating Risk

Telematics are a great way to accurately price insurance to risk. Good drivers pay less. Most of us think we’re good drivers. But are we?

Humans tend to underestimate risk, and over-estimate their own driving skills. Memory is fleeting but data lives forever.

I often talk to people who say they “have a completely clean record”, but reports show otherwise. They’re not trying to lie; they just don’t remember. That time your car was hit in the parking lot? When the deer ran in front of you? Or you had a minor fender-bender but no damage? Those are all “incidents” to insurance companies. Like it or not, they indicate a higher chance of future losses.

What I Like About Telematics

I’d probably save money. I’m a low mileage driver. I use my bike for most errands and to commute. Intellidrive allows me to pay lower insurance premiums for reduced driving.

It gives good feedback. Intellidrive records “events” that adversely affect my rates. Those can be my fault, like speeding or rapid starts. Or they could have nothing to do with how I’m driving, but when. Driving very late or during rush hour is a higher risk. This knowledge can be helpful if you want to improve your driving safety. A parent could use it to keep eyes on a teen driver. The app has videos and other driver training tips, too.

I’m a data nerd. I like to monitor my sleep and exercise with a fitness tracker. Intellidrive is like a FitBit for my driving. If you like that sort of thing, you’ll like telematics.

Downsides to an Insurance Company Monitoring App

It collects a lot of data – for an insurance company. It tracks where and when I drive. That’s useful in calculating a fair price for my insurance. It’s also valuable to others who might want to know about me. I know: my smartphone, smart speaker and my Fitbit already have a lot of data about me. I trade my privacy with those vendors in exchange for the utility of the product or service.

The insurance company owns that data.I’m sure the insurance company says “we’ll never sell your data”. But they might sell anonymized data. And data can be hacked. Or used against me if I’m in a crash or legal proceeding.

The Long Term Effect of Telematics

Attitudes about trading data for discounts are changing. More people are choosing to let auto insurers monitor their driving. As insurers gather more data, I expect higher rates for drivers who don’t choose to be monitored. There are two reasons for this:

The risk of uncertainty.Insurers set rates based on experience. Telematics allow them to project your chances of loss, tied directly to your behavior. Without that data about you, insurers will want to charge a “risk premium.”

Adverse selection. Remember the “opt out” option? If your driving score projects a surcharge, you can bail out within the first 45 days, with no rate penalty. As telematics become more pervasive, underwriters may assume that people who decline monitoring are higher risk drivers – and warrant higher rates.

Would I Sign up for Telematics?

If I could own the data,I’d be all in. I’d like to see a driving app that I control. I want to own my driving data and decide who to share it with. I expect that would cost something. You know what they say: if it’s free, you’re the product.

If I owned the data and wanted to shop my insurance, I could export a report from my app to my agent. They could check prices and recommend coverage. The insurance companies could access my scores, but not my data. That’s the kind of telematics I would sign up for.

But I may do it anyway. Privacy is an illusion in our wired society. My smart speaker probably listens a lot more than I think it does. I share my location via smartphone for the utility of real-time maps, traffic data, and more. And auto insurance is a big-ticket item. Everyone likes to save money.

Are We At the Tipping Point?

Telematics will reach a point where the cost difference will be hard to ignore. It’s probably already there for someone who drives as little as I do. And it may be for you, too, during COVID time.

Do you live in Maine and have questions about low mileage auto insurance discounts? Want to know more about Progressive Snapshot, Travelers Intellidrive or Safeco RightTrack? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We offer a choice of preferred auto insurers to help you find the right fit. We’re independent and committed to you.

Sometimes, staying apart means staying safe. That includes when you buy insurance, file a claim, and repair vehicles or property.

People value stability in uncertain times. Insurance delivers. You can do your insurance business in a low-contact, safe manner. You don’t have to sacrifice personal advice and service. Here’s how.

GET NO-TOUCH INSURANCE QUOTES

Get insurance quotes online. Most insurance agencies and companies offer online auto and home insurance quotes. Enter information about your vehicles and property and get quotes back. A good independent insurance agency can deliver several quotes at once. That helps you compare.

Get advice, not just quotes. It’s hard to know if you’re asking for the proper coverage online, or to compare the quotes you receive. That’s why most people prefer to consult an agent before they actually buy a policy. A tech-savvy insurance agent should be available by text, video or real-time chat as well as phone and email.

BUY INSURANCE REMOTELY

Read and sign documents electronically with e-mail, text and e-signature. These tools allow you to read and sign applications from anywhere. All you need is a computer or mobile device.

Use contactless payment. Most insurers accept credit cards or electronic checks using your bank account info. No need to leave home and go to the insurance office.

AVOID INSURANCE PEOPLE COMING TO YOUR HOME

Many insurers allow customers to complete a self-inspection. That usually involves answering questions about your home’s systems and emailing pictures.

In case of a claim, avoid an insurance company appraiser’s visit. Email or upload photos of your damage to the insurance adjuster.

CONTACT-FREE INSURANCE SERVICE and PAYMENTS

Use mobile apps. Most insurers have them. Download and use them to request changes, check on billing, make payments and file claims.

Don’t want to use an app? You can do many of the same things over the phone, email, video or text chat with your agent.

GET VIRTUAL INSURANCE COVERAGE REVIEWS

Modern tools allow you to meet virtually with your Insurance agent. They can even share documents with you by video. You can get personal service and answers to your questions quickly and safely, without leaving home.

DOWNLOAD INSURANCE DOCUMENTS

You don’t have to go into the insurance office to get policy documents. Here are some other ways:

Your insurance company’s app. Get documents on your mobile device.

Register for an insurance company account. Set one up and download the documents to your computer.

Use your agency account.Tech-forward insurance agencies offer online access. These allow you to view your policy information and download insurance documents.

Ask your agent to email or text your document to you.

FILE CLAIMS FROM THE SCENE

Report online. Use your insurer’s mobile app to start a claim. Or register for a free account with your insurance company, and file online.

Call your agent who can explain your coverage, answer questions and help you file a claim.

DON’T SACRIFICE PERSONAL SERVICE

One advantage of having a local agent is that we know you and live where you do. That’s more important than ever in this era of physical separation.

Noyes Hall & Allen Insurance is a forward-thinking agency. We’ve invested in tools and ideas to provide personal advice to you easily and safely. Do you prefer text, video, phone, or a combination of all? Any way, you can get a local agent’s trusted insurance advice without venturing to our office.

Are you looking for a Maine insurance agent who can serve you safely in uncertain times? Call a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. Or visit noyeshallallen.com.