An antique or classic car is fun to admire, show, drive and collect. It can also be a good investment, and a great hobby. You’ll want to insure your classic properly to protect your investment.

Your Maine Classic Car or Antique Is Unique. Your Insurance Should Be, Too.

An “off the shelf” auto policy isn’t a good fit for your classic, for these four reasons:

- Valuation – standard auto policies pay the depreciated “book value” of a vehicle. There’s a big difference between a ’78 Firebird that’s been babied and one that’s been driven hard and put away wet. Standard policies value the cherry one and the pre-restoration project the same. Collector car policies usually insure on an “agreed value” basis. You and the insurer agree on the amount to be paid on a total loss BEFORE anything happens.

- Use and Mileage – classic owners drive just a few miles a year – much less than their “daily driver”. When they do drive, it’s often a leisurely trip to the ice cream shop or rally, not a rush hour commute. “Off the shelf” policies consider all driving the same. They also assume a minimum of 8,000 miles driven per vehicle per year. Why pay full-time insurance rates for part-time insurance? Antique and classic owners pay way too much in that scenario.

- Parts – Anyone who’s scoured New England’s back roads looking for Series 1 Rover parts knows they can be expensive and hard to find. You need a policy that will pay for the right part – and maybe even help you locate it. Regular insurance policies pay for replacement parts after an accident. If your vehicle is more than a few years old, insurers usually only pay for aftermarket parts. That sends shivers down the spine of an antique buff.

- Roadside Assistance – If you break down on the way to your show, or during a rally, you want your classic worked on by a trusted mechanic. Most classic auto policies offer special flatbed coverage to get you to a mechanic qualified to work on your vehicle.

What Vehicles Qualify For Maine Classic Car Insurance?

In general, insurers define a classic car as 20 years or older, including

- Sports cars (MG, Triumph, Alfa Romeo, etc.)

- Muscle cars (Corvette, Camaro, Firebird, Mustang, etc.)

- Street rods and customized vehicles

- Collector vehicles, including antique motorcycles

- Vehicles in mid-restoration

Classic vehicle policies may limit:

- Annual mileage driven

- How it’s used (“daily drivers” usually don’t qualify)

- Young drivers

- Storage (require you to garage it when not in use)

Answers to Your Antique & Classic Insurance Questions

If you live in southern Maine and have questions about insuring your classic or antique, contact a Noyes Hall & Allen agent at 207-799-5541. We offer a choice of several insurers; let us find the right one for you. We’re independent and committed to you.

How to Get Renters Insurance in Portland, Maine

How to Get Renters Insurance in Portland, Maine

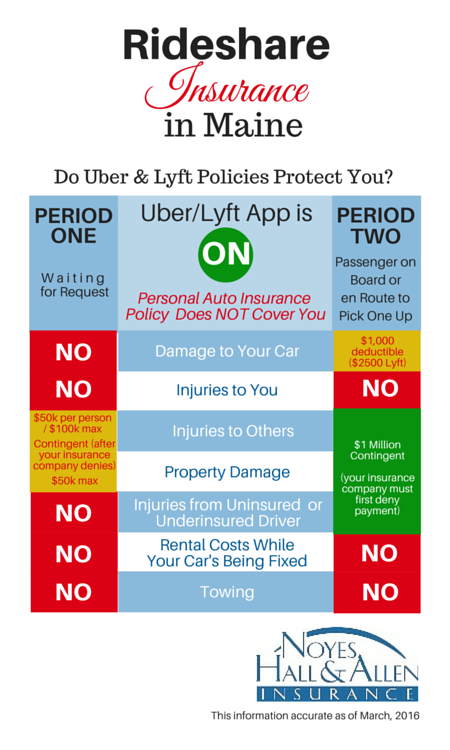

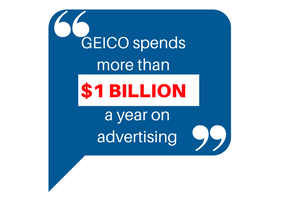

State Farm, Geico, Allstate and Progressive all sell directly from company to consumer via the internet and inbound call centers. If you contact them, remember that you’re talking to an insurance company employee. You’re accessing information prepared, controlled and presented by the insurance company. Expect that they will look out for their own business interests first.

State Farm, Geico, Allstate and Progressive all sell directly from company to consumer via the internet and inbound call centers. If you contact them, remember that you’re talking to an insurance company employee. You’re accessing information prepared, controlled and presented by the insurance company. Expect that they will look out for their own business interests first.